A summary of Finance for Actuarial course:

- Cash Flows; Time & Rounding Conventions; Glossary of (some) Financial Products

- Simple & compound interest; Rate of Discount; Nominal Interest; Accumulation Factors; Force of Interest

- Discounted, Accumulate & Present Value; Continuous Cash flows.

- Annuties Immediate & Due; present and future values; increasing & perpetuities…

- Loan schedules; Level Installments; APR and Flat rate

- Equations of Value and Yield.

(This covers about half of the Institute and Faculty of Actuaries CT1 exam — though you should probably work on context if you want to pass the exam.)

Cash Flow

Def [Cash flow] A cash flow is a vector of times

, (t_2,c_2), ... (t_n, c_n) \Big)")

If

We will generally consider the values of

Time

Def [Exact number of days] The exact number of days between two dates is the number days from the first given date to the second (excluding the first or last date)

E.g. There are

Def [The Simplified Convention] The simplified convention assumes every month has 30 days and every year has 360 days. So under the simplified convention the number of days between two dates

+ 30 ( m_2 - m_1 ) + 360 (y_2 - y_1 )")

Q. How many days are there between 29th April and 20th September under the simplified convention?

A. 141.

Rounding

Numbers are often rounded so that they fit with natural units, or so they are simpler (and thus hopefully reduce human error). There are no fixed rules for rounding and you need to be mindful of “round off error”, as many small errors can add up!

Here are some rules of thumb

- Number in currency are rounded to the nearest hundredth.

- Number in currency larger than 100,000 are rounded ot the nearest one.

- General numbers of modulus less that 1 are rounded to the nearest tenthousandth.

- General numbers with modulus larger that 100,000 are rounded to the nearest hundredth.

A Glossary of financial products

Here is an imcomplete and perhaps simplified list of finacial products. Some are risky and some are risk-free. All of these are examples of cash flows.

Savings account: A deposit in a band that recieves interest. Often recieves fixed interest, at least for an initial period.

Bond: After purchase, you receive regular payments called coupon payments and on a specific date of maturity you receive an amount of money called the par value or face value of the bond.

Zero-coupon bond: A bond without coupons. (face value is typically higher than purchase price).

Share: A unit of ownership in a public company (aka a coperation).

Annuity: A contract sold by an insurance company. After making one or more payments to a purchase the annuity. The buyer recieves periodic payments unit death (basically this is a pension).

Interest only Loan: The borrower is paid an amount of money. The borrower pays interest on regular invervals at maturity the full amount is due back. (Similar to a bond but the rights are different).

Repayment Loan: The borrower is paid an amount of money. He repays the full amount plus interest in a series of periodic payments.

Interest Rates

When you deposit money in a savings account, in reture over time you recieve payments per unit of money saved. This is called interest. In general interstes rates can be fixed (for a time-period) or variable. Rates depend heavily on the economic states at the time the savings account is initiated.

Def [Effective rate of interest / AER] if

Def [Simple Interest] Simple interest is added over time. In particular, under simple interest, an initial capital

+ ... c i (n-1)")

after

Suppose that interest is fixed over time

Simple interest is rarely used in practice. Really you earn interest on your interest, so called compound interest. Unless stated otherwise when we say interest we mean compound interest.

Def [Compound Interest] Compound interest is multiplied over time. In particular, under compound interest, an initial capital is returned as

)...(1+i(n-1)).")

Ex. Suppose that interest is fixed over time

^n.")

Rate of Discount

Def [Rate of Discount] You are loaned

( 1+ i) =1")

Here

Ex. Show that

Nominal Rates

So far (fixed) interest is compounded as

^t")

where

Def [Nominal Rate of Interest] Over a time interval of length

then

Ex. Show that, under fixed interest, that  = (1+i)^h\quad\text{and}\quad i_h = \frac{(1+i)^h - 1}{h} \ .")

Ex. [Nominal Rate of Discount] Argue that if there is a notion of nominal discount,

(1 + h i_h) =1 \quad \text{and} \quad d_h = \frac{i_h}{1+ h i_h}.")

Accumulation Factor

Thus far interest has been applied in units or fractions of time. With Accumulation factors, we have a working definition of compounding any time length.

Def [Accumulation Factor] If

")

then

Lemma [Principle of Consistency] Any self respecting Accumulation factor must satisfy

= A(t,t') A(t',t'')")

for

Force of Interest

The Accumultion factor is great; it considers nice and general time, but it is a multaplicative factor not a rate of change. For this we consider the Force of Interest.

Def [Force of interest] Assuming the following limit exists

= \lim_{h\rightarrow 0} \frac{1}{h} \left[A(t,t+h) -1 \right]")

then we call

Note that the above defintion assumes that our Accumulation factor has nice differentiability properties. (This is a limitation.)

Ex. If

Ex. If there is a fixed rate of interest ") (Hint: Differentiate

(Hint: Differentiate

Thrm. The Accumulation factor relates to the force of interest as follows  = \exp \left\{ \int_s^t \delta (u) du \right\}")

This result is really just the Fundamental Theorem of Calculus applied to the

Discounting and Accumulating

We consider how to evaluate several payments made at different times at a single moment in time.

Def [Discounted Value and Accumulated Value] A cash flow Consider a cash flow

,...,(t_n,c_n))")

where for each

- For

, the Discounted Value of the cash flow is

= \sum_{i=1}^n \frac{c_i}{A(s,t_i)}")

where

- For

,

is called the Present Value of the payment.

- For

= \sum_{i=1}^n c_i A(t_i,s)")

Note in each case above we essentially relativize money to a single time. From this we can move to different times:

Ex. Argue that for

A(s,r) = \text{DVal} ( \bar{c},r)")

and find a similar expression between

Continuous Cash Flow

Def [Continuous Cash Flow] A continuous cash flow over time interval ![[a,b]](https://s0.wp.com/latex.php?latex=%5Ba%2Cb%5D&bg=ffffff&fg=1a1a1a&s=0&c=20201002)

For a continuous cash flow and

= \int_a^b c_c(u) \frac{1}{A(s,u)} du \quad\text{and}\quad AVal(c_c,t) = \int_a^b c_c(u) A(s,u) du")

I’ve called this a theorem as is really just a consequence of the definition for discrete cash flows.

Def [Continuous payment on fixed capital] If you have a fixed amount

= c \delta(t)")

Ex. Convince yourself that the continuous payment of interest above agrees with the interest accrued under fixed interest (and fixed force of interest).

Ex. Convince yourself that if cash flow

(Nb. these cash flows could be discrete or continuous, or indeed, a mixture of the two) then argue that

&= \text{DVal}(\bar{c}_1, s) + \text{DVal}(\bar{c}_2, s) \\ \text{AVal}(\bar{c}, t) &= \text{AVal}(\bar{c}_1, t) + \text{AVal}(\bar{c}_2, t)\end{aligned}")

where is assumed that

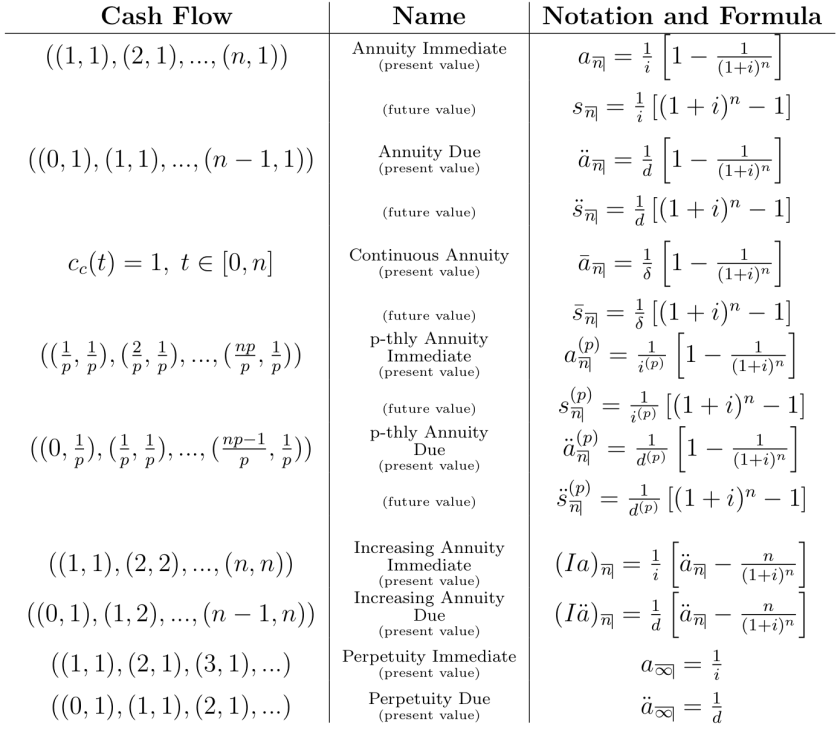

Annuities

Annuities are cash-flows consisting of regular payments.

Def [Annuity Immediate] An Annuity Immediate is the cash flow

,(2,1),...,(n,1))")

and its present value and future values respectively satisfy

,\qquad s_{ \actuarialangle{n} } = AVal(\bar{c} , n )")

Show that, under fixed interest,

^n} \right)")

We could continue writing a bunch of definitions on annuities. Instead here is a big table

Ex. Convince yourself in the table above that for each present value we get the future value by multiplying by

^n a^{(p)}_{\actuarialangle{n}} = s^{(p)}_{\actuarialangle{n}}")

Ex. Convince yourself in the table above to go from an annuity due to and annuity immediate we multiply by

Loan Schedules

In taking a loan, the amount that you take our should equal the amount that you put in, after adjusting for interest. Thus if you take a loan of

")

Def [Level Installments] You pay a loan back with level installments if all repayments on your loans are equal. I.e.

, ..., (n,x))")

This is an annuity immediate i.e.

Ex. Argue by the same logic as above, that if

Ex. Convince yourself that it is common sense that the interest and capital paid on the loan at year

Ex. Convince yourself that if the Loan is repaid by a general repayment schedule

APR

Def [Annual Percentage Rate of Charge] Suppose that you arre given a loan

")

where the subscript

Note: that after substitution

&= \frac{c_1}{1+i} + \frac{c_2}{(1+i)^2} + ... + \frac{c_n}{(1+i)^n} \\ & = c_1 x + c_2 x^2 + ... + c_n x^n.\end{aligned}")

In other words we have a polynomial. So finding the APR resorts to us finding roots of a polynomial, which is analytically non-trivial but, in practice, numerically straight-forward – just ask wolfram-alpha!

Def [Flat rate] The flat rate of a loan is

The flat rate is a bit like APR, except it judges the absolute change in capital per unit of loan. However, capital changes relatively (not absolutely) so people tend not to use the flat rate.

Equations of Value

We apply the same logic that we used to get the APR of a loan to general cash flows.

Def [Equation of Value / Yield] For a cash flow the equation

")

is called the Equation of Value. If there is a unique solution

Note: The yield belongs to the interval

&= c_0 + \frac{c_1}{1+y} + \frac{c_2}{(1+y)^2} + ... + \frac{c_n}{(1+y)^n} \\ & = c_0+c_1 x + c_2 x^2 + ... + c_n x^n= 0\end{aligned}")

A yield of zero, suggests that payments in the cash flow are neither growing of shrinking. A positive yield suggests that payments are growing (at rate