The Weighted Majority Algorithm is a randomized rule used to learn the best action amongst a fixed reference set.

We consider the following setting

- There are a fixed set of actions

which one may choose. There are a set of outcomes

.

- After choosing an action

, an outcome

occurs and you receives a reward

. Over time a policy

chooses actions

and outcomes

,

- It is assumed that the function

is known by the policy.

- The accumulated a net reward is

:=\sum_{t=1}^T r(\pi_t,y_t).")

We are interested in how our dynamic policy

- For this reason, we consider the regret of policy

:=\max_{i=1,...,N}\left\{ \rho(i,T) -\bE \rho(\pi,T)\right\}.")

- We can only retrospectively find the best fixed policy, whilst our policy

quantifies how we regret not having had the information to have chosen the best fixed policy.

- Note a ‘good’ policy would have low regret. For instance, we might hope our dynamic policy is as good as the best fixed policy, i.e.

.

Using Blackwell’s Approachability Theorem, we saw that low regret policies exist. See Section [Blackwell]Theorem [blackwell:regret]. One of the key advantages of such algorithms is that is does not place statistical assumptions on the outcome sequence

Weighted Majority Algorithm

For parameter

We can derived the following regret bound

Theorem: If policy

(1) With

\leq \eta^{-1} \log(N) + \frac{\eta T}{2},")

for choice

\leq 2\sqrt{2T \log(N)}.")

(2) For

\geq \frac{1 }{1-e^{-\eta}} \left\{ \eta \max_{i=1,...,N} \rho(i,T) +\log N\right\}.")

(3) For

\leq \eta_T^{-1} \log(N) + \frac{1}{8} \sum_{t=1}^T \eta_t,")

for choice

\leq \sqrt{ T \log N}") •

•

Proof:

(1) Observe

In the second inequaltiy, we apply the Azuma-Hoeffding Inequality, see Section [Azuma]. Taking logs and rearranging, we gain the required expression . Substituting

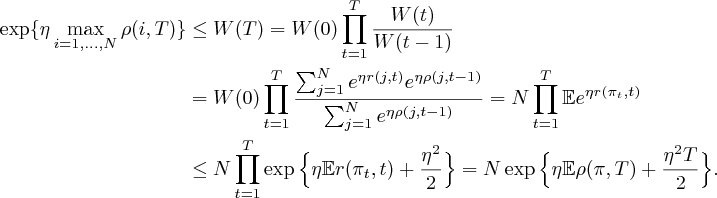

(2) We note the following inequality holds

} \leq \bE [ (e^\eta -1)r(\pi_t,t) +1 ] \leq \exp\{ (e^{\eta}-1) \bE r(\pi_t,t)\}.")

In the first inequality, we bound with the line segment above the exponential. In the second inequality, we apply the bound

\} \leq N \prod_{t=1}^T \bE e^{\eta r(\pi_t,t)} \leq N \exp\{(e^{\eta}-1) \bE \rho(\pi,T) \}.")

Taking logs and rearranging gives the required bound.

(3) The crux of the proof (1) was that the function

We can express our weights differently, notice,

= \frac{\frac{1}{N}s_{i,t-1}^{\eta_t/\eta_{t-1}} }{\frac{1}{N} \sum_{j=1}^N s_{j,t-1}^{\eta_t/\eta_{t-1}}},\qquad \text{where}\qquad s_{i,t-1} & = \exp\left\{-\eta_{t-1} \rho(i,t-1) + \eta_{t-1} {\mathbb E} \rho(\pi, t-1) - \frac{1}{8}\eta_{t-1}\sum_{k=1}^{t-1} \eta_k \right\}\\ \text{and}\qquad\quad S(t) & = \frac{1}{N} \sum_{i=1}^N s_{i,t}.\notag \end{aligned}")

^{\frac{1}{\eta_t}} % &\leq \left( \frac{1}{N} \sum_{j=1}^Ns_{j,t-1}^{{\eta_t}/{\eta_{t-1}}}\cdot e^{-\eta_t r(j,t) + \eta_t\bE r(\pi_t,t) - \frac{\eta_t^2}{8}} \right)^{\frac{1}{\eta_t}} \\ % & = \underbrace{\Bigg( \bE e^{-\eta_t r(\pi_t,t) + \eta_t (\bE r(\pi_t,t)) - \frac{\eta_t^2}{8}}\Bigg)^{\frac{1}{\eta_t}} }_{\leq 1, \text{ by Azzuma-Hoeffding}} \times \underbrace{ \left( \frac{1}{N} \sum_{j=1}^N s_{j,t-1}^{\eta_t/\eta_{t-1}}\right)^{\frac{1}{\eta_t}}}_{\leq S(t-1)^{\frac{1}{\eta_{t-1}}} \text{ by Jensen's Ineq}} \leq S(t-1)^{\frac{1}{\eta_{t-1}}} \end{aligned}")

Since